Personal finance is the most important part of life; if it is not managed on time, then money can not be controlled with high debt issues. Therefore, future precautions need to be adopted to control unnecessary expenditure of money on useless items. If these personal finance tips are implemented in life before getting involved in high debt, then people can easily manage money.

1. Importance of Improving Personal Finances

If you want to improve your personal finances, you must first gain full control over your expenses, income, savings, and investments. Creating a budget, avoiding wasteful spending, and focusing on long-term financial goals are essential to improving personal finances.

2. Track Your Monthly Income and Expenses

First of all, you have to keep track of your expenses or your income on a monthly basis, where your expenses are going, and where you are spending. Now that expense is not going to be excessive, or there is no extra deduction from it, and then you have to follow these things to control your expenses or to control the necessary expenses.

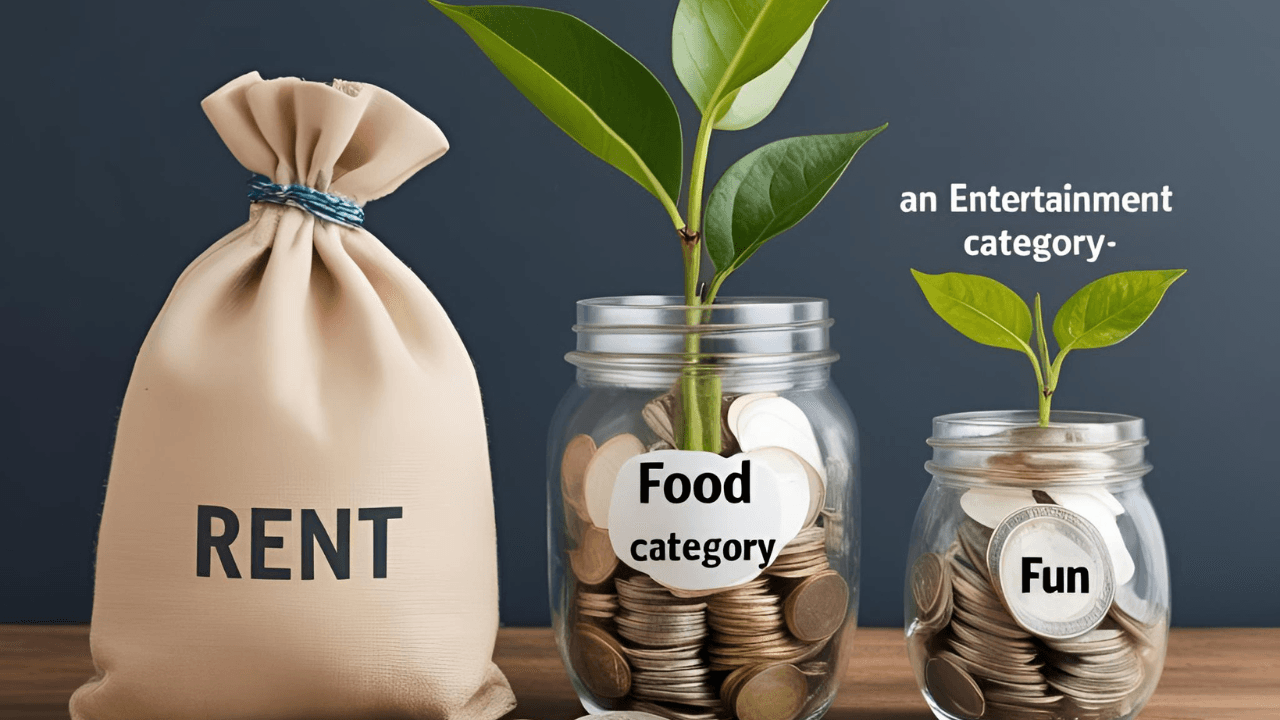

3. Create a Spending Plan with Categories

After that, you have to make a plan in which you have to create categories: a rent category, a food category, and an entertainment or fun category. What will you do in it, and how much do you allocate to each category? Then you will not spend extra money. You will manage your budget within this circle, and the money you have will be saved from going into any debt.

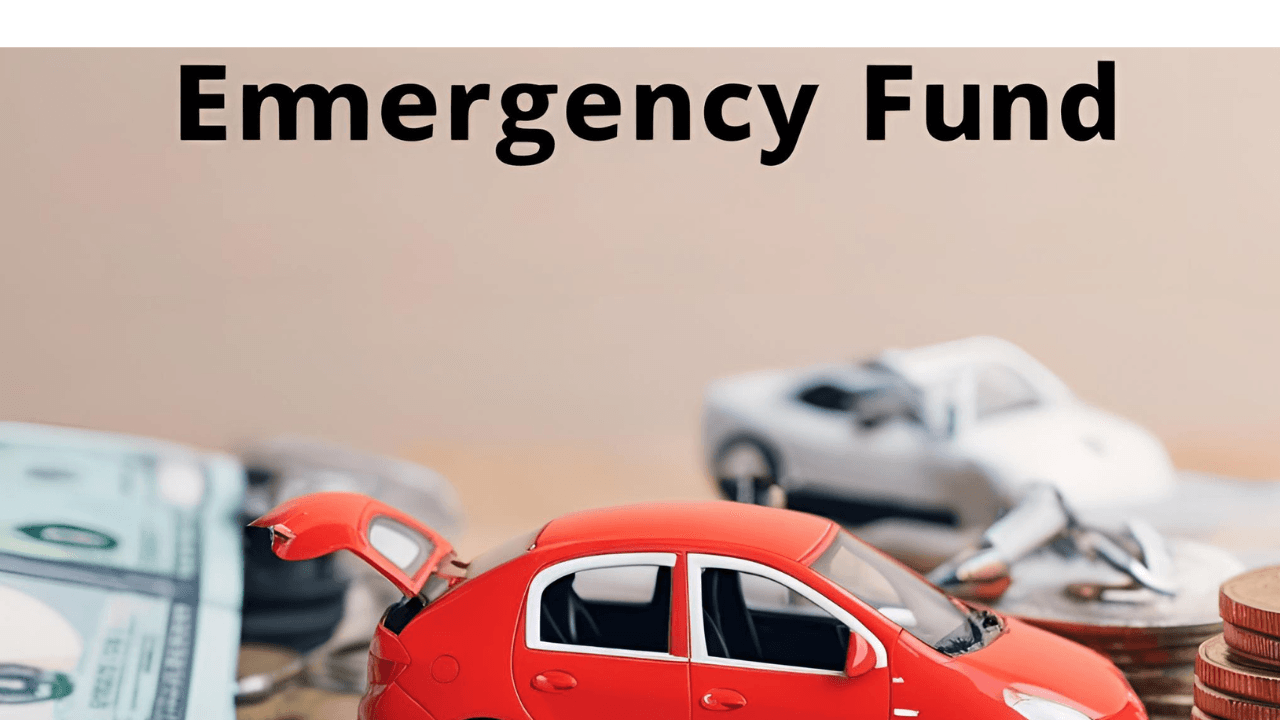

4. Build an Emergency Fund

You also have to set aside an emergency fund. Just like your unexpected expenses, like health issues, medical expenses, etc., are set aside. And if your car breaks down or needs to be repaired or there is any other kind of damage that you have to spend outside of your routine, then you have to keep some savings for that. For example, you can create a savings account for a three- to six-month living course, a savings account in which you save so that you can manage these things at the same time.

5. Focus on High-Interest Debt First

After that, you have to manage your high-interest debt first. That means, just like you have a credit card bill, you have to pay it. You have to pay first so that you do not have to pay more interest and do not go into debt; then you can avoid debt in this way. Do not adopt the small interest rate first. First, adopt the one with high interest so that your income remains safe and you can manage it.

6. Automate Your Savings

You have to make your account automatic, which will mean that you will fix some money that will be going into your savings account every time. This will then create a savings for you, and you will be able to save your time. You will also gain discipline, and you will be able to group your savings.

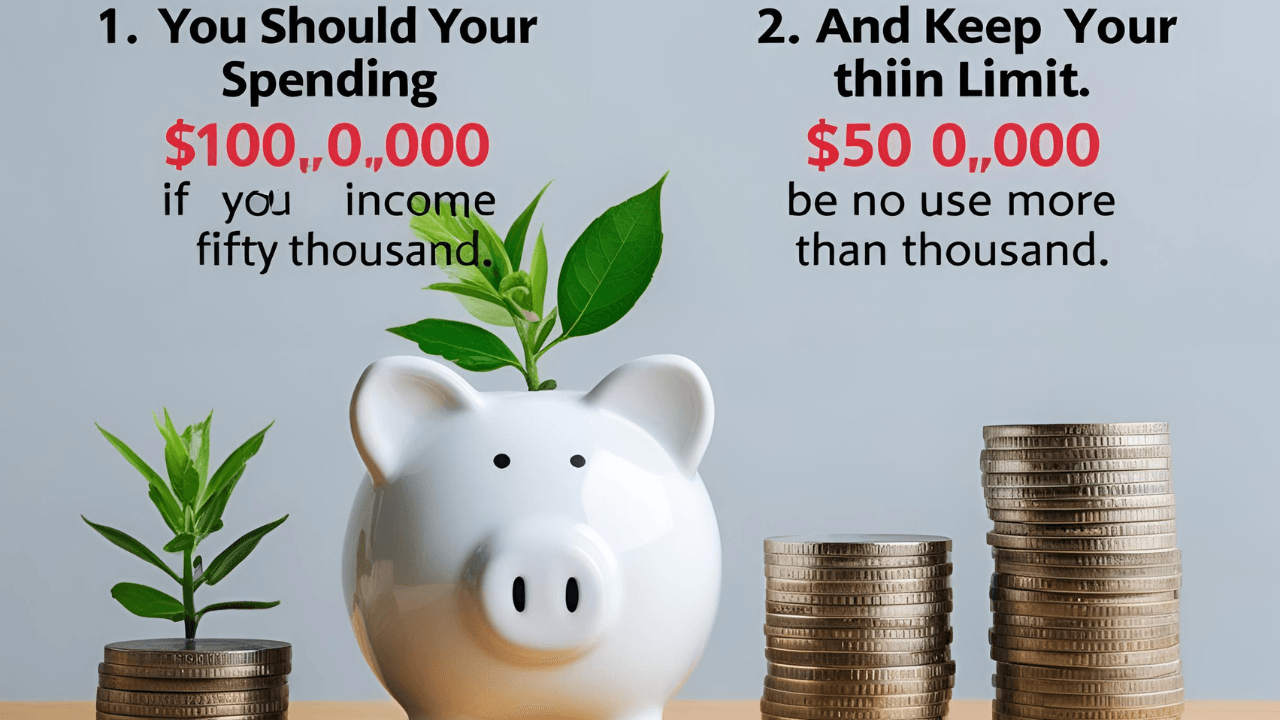

7. Spend Within Your Limits

And the second is that you should keep your spending within your limit. For example, if your income is fifty thousand, then you should not spend more than fifty thousand. This will mean that you will be able to use the necessary debt, and this will help you a lot in personal finance.

Pingback: Fact Check: Lies Detected | Indo Pak Information Standoff

Pingback: Finance vs Lease: Which is the Better Way to Get a Car?